Forbearance student loan meaning is more than just a financial term—it’s your lifeline when payments get tough. Many borrowers stumble over this concept, unsure if it will help them or make their debt worse. Understanding it correctly can save you from unnecessary stress and costly interest, giving you peace of mind in your repayment journey.

Even if you’re new to student loans, knowing how forbearance works in real life is empowering. From temporary payment pauses to interest implications, this guide breaks it down simply and clearly. By the end, you’ll feel confident managing your loans, knowing exactly when forbearance is a smart move—and when it might backfire.

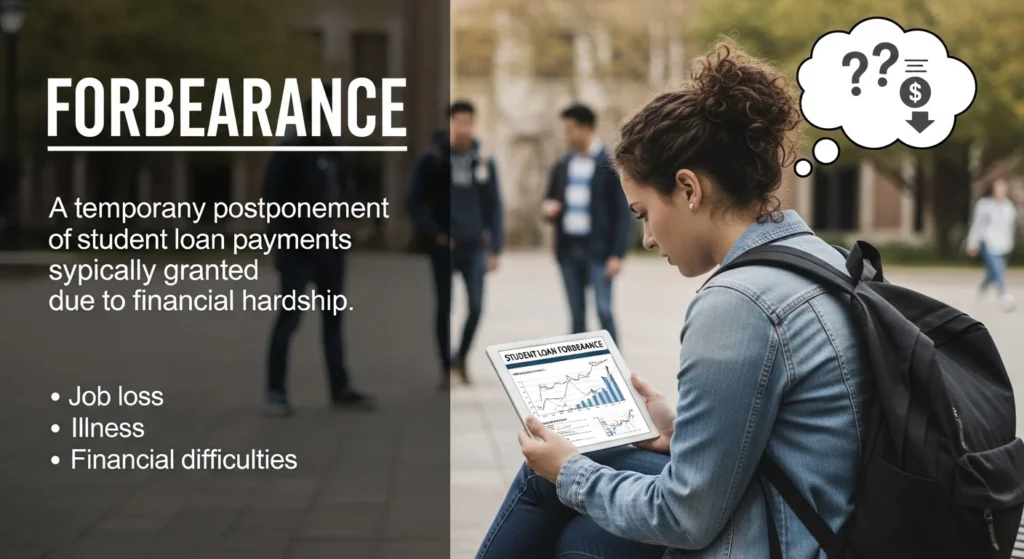

What Does “Forbearance” Mean in Student Loans?

In the context of student loans, forbearance is a temporary pause or reduction in your loan payments granted by your lender. Unlike loan forgiveness, it doesn’t erase what you owe—it simply gives you breathing room to manage your finances.

Key Points About Student Loan Forbearance:

Temporary Relief: Payments can be paused or lowered for a set period.

Interest Accrues: Even if your payments are paused, interest usually continues to accumulate.

Eligibility: Generally available to borrowers facing financial hardship, medical issues, unemployment, or other challenges.

Types: Can be discretionary (lender decides) or mandatory (government requires under certain conditions).

Origins of the Term

The word forbearance comes from the idea of “refraining from action.” In lending, it dates back decades and was originally a legal term describing a lender’s patience with a borrower who can’t pay on time. Online forums and financial blogs today often discuss forbearance in plain English, making it easier for borrowers to understand without legal jargon.

How People Use Forbearance in Real Conversations

Borrowers frequently discuss forbearance on Reddit, Discord, Instagram, and student loan Facebook groups. Here’s how it typically comes up:

Texting Friends: “I had to put my loans in forbearance until my internship starts.”

Financial Advisor Chat: “You might qualify for a discretionary forbearance if your income drops.”

Dating or Casual Talk: Sometimes jokingly referenced as “my student loans are on a nap,” but serious in financial discussions.

When It’s Appropriate vs. Awkward

Appropriate: Discussing repayment options with your lender, financial advisor, or support group.

Awkward: Bragging about being in forbearance to friends; it’s meant as a temporary aid, not an achievement.

Real-Life Examples of Forbearance in Student Loans

Here are some short, relatable examples of forbearance student loan meaning in action:

Texting a Friend:

“Hey, I put my loans in forbearance for 6 months. Finally, a break!”

(Meaning: Payments are paused temporarily, but interest still accrues.)

Explaining to a Parent:

“I’m on a forbearance plan right now because I lost my part-time job.”

(Shows eligibility due to financial hardship.)

Reddit Post:

“Mandatory forbearance saved me while I was deployed. Interest keeps growing though.”

(Highlights government-mandated forbearance.)

Financial Advisor Chat:

“Discretionary forbearance might help if you can’t make your full payment this month.”

(Shows lender-based approval.)

Casual Group Chat:

“My student loans are in forbearance, so I’m treating myself a little.”

(Emphasizes temporary relief, not forgiveness.)

Common Mistakes & Misunderstandings

Even experienced borrowers sometimes confuse forbearance with other student loan terms.

Top Misconceptions:

Confusing Forbearance with Deferment: Deferment may stop interest for certain loans; forbearance usually doesn’t.

Thinking Debt Disappears: Payments are paused, but the debt still exists, plus accrued interest.

Wrong Context Use: Using forbearance casually in chats without understanding implications can mislead friends.

Related Slangs & Abbreviations in Financial Chat

If you’re learning forbearance student loan meaning, it helps to know similar terms:

Deferment: Temporary pause on payments, sometimes interest-free.

Grace Period: Time after graduation before payments start.

Income-Driven Repayment (IDR): Payments based on your income level.

Default: Failure to repay loans, which harms credit.

FAQs About Forbearance in Student Loans

1. What is the difference between forbearance and deferment?

Forbearance usually allows temporary payment reduction or pause but accrues interest, while deferment may sometimes prevent interest from accruing, depending on your loan type.

2. Can I enter forbearance multiple times?

Yes, many lenders allow repeated forbearance periods, but each instance may increase accrued interest.

3. Does forbearance affect my credit score?

Typically, no—entering forbearance does not count as a missed payment. However, unpaid interest still grows.

4. How long can student loans stay in forbearance?

It depends on your loan and lender. Federal loans often allow 12 months per request, sometimes renewable. Private lenders vary.

5. Should I choose forbearance over an income-driven repayment plan?

It depends on your financial situation. Forbearance is temporary relief, while IDR can provide ongoing lower payments without pausing interest.

Conclusion

Understanding forbearance student loan meaning is crucial if you want to manage your student debt effectively. While it provides temporary relief, it doesn’t eliminate your obligation, and interest still accumulates. Using this guide, you now know the definition, real-life examples, common mistakes, and related terms, so you can make informed choices in 2026 and beyond.

What’s your favorite chat abbreviation or financial slang? Drop it in the comments!